W ostatnich latach coraz więcej osób odkrywa korzyści, jakie niesie ze sobą nowe polskie kasyno online. Te witryny stają się niezwykle popularne w Polsce, oferując zróżnicowane gry oraz atrakcyjne promocje. W tym artykule zyskasz wiedzę na temat, new casino bonus co warto wiedzieć o nowych polskich kasynach online oraz jak wybrać odpowiednie dla Ciebie.

Dlaczego Warto Spróbować w Nowym Polskim Kasynie Online?

Nowe polskie kasyna online obalają stereotypy graczy z licznych powodów. Oto kilka najważniejszych elementów, które warto przemyśleć:

Wielka oferta gier: Nowe platformy często oferują rozległy wybór gier, od klasycznych automatów po stoły do gry w pokera czy ruletkę.

Atrakcyjne bonusy: Nowe kasyna często oferują wielorakie promocje, które mogą wliczać bonusy powitalne oraz bezpłatne spiny.

Bezpieczne środowisko: Takie kasyna funkcjonują na podstawie aktualnych regulacji prawnych, co zapewnia bezpieczeństwo i uczciwość w grach.

Jak Odnaleźć Nowe Polskie Kasyno Online?

Wybór idealnego nowego polskiego kasyna online może być wyzwaniem, szczególnie przy tak dużej konkurencji. Oto kilka kluczowych porad:

Sprawdź licencję: Upewnij się, że kasyno ma ważną licencję, która zapewnia jego legalność i bezpieczeństwo.

Przeczytaj opinie: Zasięgnij zdania innych graczy. Recenzje mogą przynieść cennych informacji o jakości obsługi klienta i wypłatach.

Oferta gier: Upewnij się, czy kasyno oferuje ulubione przez Ciebie gry, a także aktualne tytuły i dostawców oprogramowania.

Bezpieczeństwo i Łatwość Gry w Nowym Polskim Kasynie Online

Kiedy uczestniczysz w nowe polskie kasyno online, bezpieczeństwo Twoich danych i przelewów jest kluczowe. Najwięcej kasyn posługuje się nowoczesnymi technologiami zabezpieczeń, aby umożliwić informacje dane graczy. Przy tym, dużo z nich przygotowuje zróżnicowane metody płatności, co zwiększa wygodę korzystania z witryny. Możesz realizować wpłat i wypłat za pomocą kart kredytowych.

Podsumowanie

Nowe polskie kasyno online to doskonała propozycja dla tych, którzy szukają świeżych doświadczeń w świecie gier. Dzięki szerokiej ofercie gier, atrakcyjnym bonusom oraz bezpiecznemu środowisku, są one w stanie spełnić potrzeby zarówno świeżych graczy, jak i weteranów. Pamiętaj, aby dokładnie ocenić kasyno przed stworzeniem konta, aby cieszyć się pełnią rozrywkowych możliwości, jakie zapewniają. Zabijaj czas odpowiedzialnie i czerp radość dobrze!

The global proteomics market is projected to be valued at USD 44.79 billion in 2025 and is expected to reach USD 134.82 billion by 2035, registering a CAGR of 11.7% during the forecast period. This expansion is driven by the escalating demand for personalized medicine, advancements in mass spectrometry technologies, and increased investments in proteomics research.

The proteomics market is experiencing robust growth as researchers and industries increasingly focus on understanding protein structures, functions, and interactions. Proteomics, the large-scale study of proteins, plays a crucial role in diagnostics, drug development, and disease management. As biological research shifts toward personalized medicine, the demand for advanced proteomic tools and technologies is escalating.

The proteomics market is evolving due to rising investments in pharmaceutical and biotechnology research.

Technological advancements in mass spectrometry and chromatography are expanding the capabilities of proteomics.

Increasing prevalence of chronic diseases and the need for targeted therapies are pushing the boundaries of this market.

With applications ranging from cancer biology to biomarker discovery, the proteomics market holds promising potential for transforming healthcare outcomes globally.

Several trends are shaping the future of the proteomics market, driving innovation and adoption across sectors.

Integration with artificial intelligence (AI): AI and machine learning tools are being utilized to process complex proteomic data faster and more accurately.

Single-cell proteomics: The ability to analyze proteins at a single-cell level is creating new research possibilities in immunology and oncology.

Label-free quantification methods: These are gaining popularity due to their efficiency and reduced sample preparation time.

Miniaturized devices and microfluidics: Portable systems for proteomic analysis are making real-time diagnostics more accessible.

These trends highlight how the proteomics market is not only expanding but also transforming in terms of tools, techniques, and applications.

Challenges and Opportunities

While the proteomics market is poised for rapid growth, it also faces significant challenges that must be addressed to unlock its full potential.

Challenges:

High cost of instruments and reagents remains a barrier for many research institutions.

Data complexity and analysis are major concerns, especially in large-scale studies.

Limited standardization across laboratories makes result comparison difficult.

Opportunities:

Rising demand for personalized medicine creates a robust need for proteomics in clinical diagnostics.

Government funding and support for life sciences research is growing globally.

Collaborations between academia and industry are fostering innovation and expanding the market’s reach.

The proteomics market, while complex, offers tremendous opportunities for stakeholders willing to invest in overcoming its inherent challenges.

Key Points:

The proteomics market is expected to witness significant growth over the next decade.

Advancements in analytical tools such as mass spectrometry are boosting data precision.

Collaborations and strategic partnerships are common among leading companies.

Increasing focus on early disease detection is driving adoption in clinical labs.

Rising awareness of proteomics applications in agriculture and food science is opening new market avenues.

Key Regional Insights

Geographically, the proteomics market displays varied growth patterns depending on infrastructure, funding, and research priorities.

North America leads the proteomics market due to strong R&D investments, a well-established biotech industry, and favorable government initiatives.

Europe follows closely, driven by a collaborative scientific community and emphasis on life sciences.

Asia-Pacific is emerging rapidly, particularly in countries like China, India, and South Korea, where healthcare modernization and research funding are on the rise.

Latin America and Middle East & Africa are slower adopters but are showing increasing interest as awareness and investment grow.

These regional differences present unique opportunities for market expansion and localization strategies.

Top Companies

The proteomics market is highly competitive, with several players making notable contributions through innovation and global reach.

Thermo Fisher Scientific offers a wide range of instruments and reagents used in proteomic research.

Agilent Technologies provides high-throughput analytical platforms tailored for proteomic workflows.

Bruker Corporation is known for its cutting-edge mass spectrometry technology.

Bio-Rad Laboratories delivers software and consumables essential for protein analysis.

Danaher Corporation owns multiple subsidiaries that contribute to the proteomics landscape.

These companies are not only driving technological advancements but also expanding market accessibility through collaborations and acquisitions.

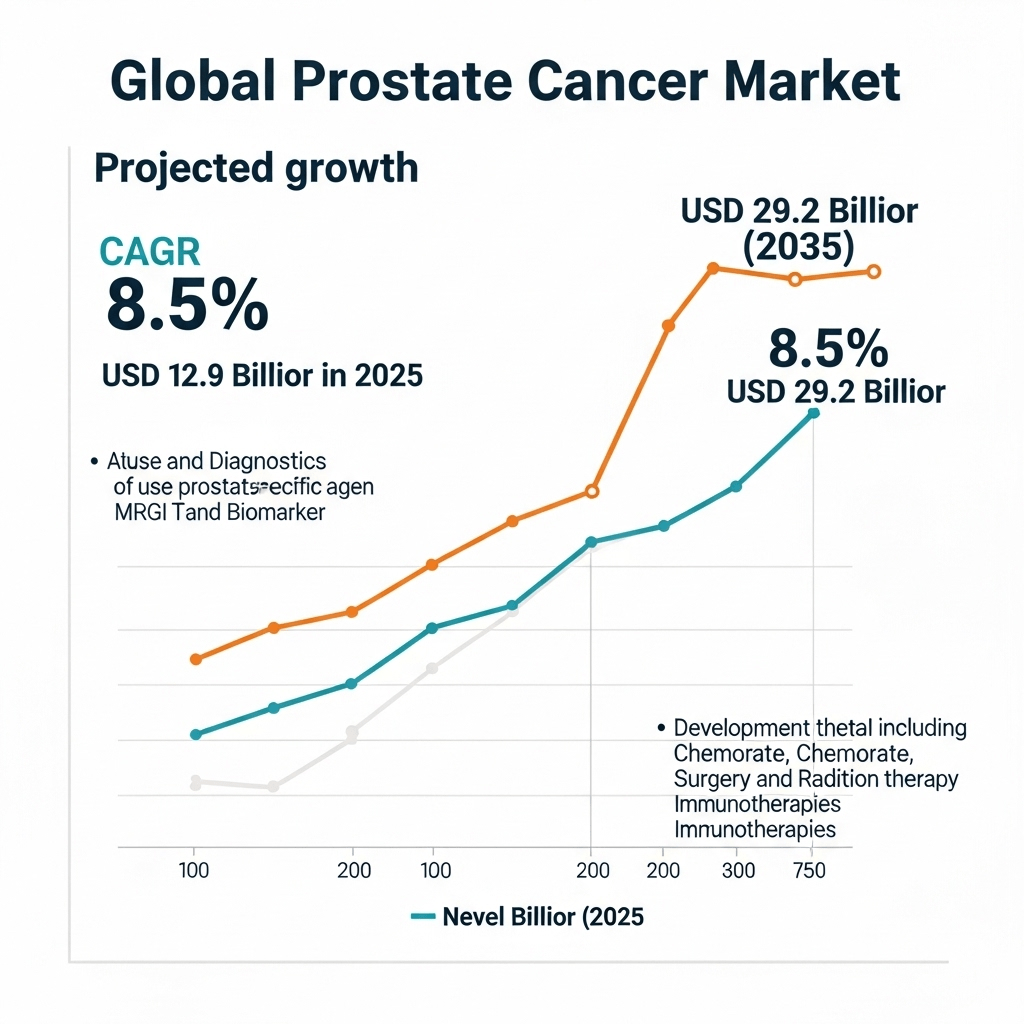

The global prostate cancer market is projected to be valued at USD 12.9 billion in 2025 and is expected to reach USD 29.2 billion by 2035, registering a CAGR of 8.5% during the forecast period, driven by advancements in diagnostics and therapeutics.

The prostate cancer market has emerged as a major focus area in the global healthcare landscape. With an increase in the aging population, particularly in developed nations, the prevalence of prostate cancer continues to rise. This has led to substantial investments in early detection methods, treatment innovations, and improved patient management systems. The market is characterized by rapid technological advancement, a growing awareness about prostate health, and the increasing adoption of personalized medicine.

Prostate cancer remains one of the most commonly diagnosed cancers in men. This has prompted medical research institutions and pharmaceutical companies to prioritize advancements in hormone therapy, immunotherapy, and diagnostic tools. As awareness and screening initiatives expand, the prostate cancer market is expected to experience sustained growth over the coming years.

The prostate cancer market has seen consistent expansion, fueled by innovations in drug development and diagnostic imaging. Several factors contribute to the ongoing growth trend, including an aging global population and higher public awareness about early screening options.

The market is projected to grow at a steady CAGR over the next five to ten years.

Precision medicine and gene-based treatments are reshaping how prostate cancer is managed.

Digital health technologies and telemedicine platforms are increasingly used for patient monitoring and consultation.

Countries with robust healthcare systems are seeing faster adoption of newer therapies.

Clinical trials are being accelerated due to collaborations between public health agencies and pharmaceutical companies.

Emerging economies are also beginning to invest in better healthcare infrastructure, opening new growth avenues for the prostate cancer market.

Challenges and Opportunities

Despite its promising growth, the prostate cancer market faces several hurdles. One major challenge is the high cost of advanced treatments and therapies, which can limit access for patients in low- and middle-income countries. Furthermore, differences in healthcare systems and regulatory approval timelines often slow the adoption of new drugs and devices.

Key Challenges:

High treatment costs and limited reimbursement options

Lack of uniform screening protocols globally

Late-stage diagnoses in underdeveloped regions

Limited access to clinical trials for patients in rural or underserved areas

Opportunities:

Rising government funding for cancer research

Expanding telehealth solutions that improve access to specialists

Development of non-invasive diagnostic tools

AI-based platforms enhancing early detection accuracy

With continued focus on research and collaboration, the prostate cancer market is well-positioned to overcome current barriers and tap into new growth opportunities.

Market Share by Geographical Region

The global prostate cancer market is largely concentrated in North America and Europe, where early detection programs and healthcare spending are more advanced. However, emerging markets in Asia-Pacific and Latin America are quickly gaining traction.

North America: Holds the largest share due to advanced healthcare infrastructure, high awareness, and active R&D.

Europe: Benefits from supportive government policies and strong investment in healthcare innovation.

Asia-Pacific: Expected to experience the fastest growth due to increasing healthcare investments and rising cancer incidence.

Latin America and Middle East & Africa: Though currently smaller markets, improving healthcare access is helping to drive market entry and growth.

Market players are increasingly targeting these regions through strategic partnerships, local clinical trials, and pricing models tailored to the local economic environment.

Top Companies

Several key players dominate the prostate cancer market, offering a wide range of treatment options and diagnostic tools. These companies are investing in new product development, strategic acquisitions, and global expansion to maintain their competitive edge.

Pfizer Inc.: Known for its development of hormone therapies and cancer-targeting drugs.

Johnson & Johnson: Offers advanced pharmaceuticals and medical devices for prostate cancer treatment.

AstraZeneca: Actively involved in prostate cancer drug development and personalized medicine.

Bayer AG: Focuses on radiopharmaceuticals and oncology-based drug research.

AbbVie Inc.: Known for its strong pipeline of oncology treatments and clinical trials.

Sanofi: Involved in immunotherapy research and new treatment pathways.

These companies are also forming partnerships with biotech startups and research institutes to enhance their portfolios and speed up innovation.

The prostate cancer market is segmented by treatment type, diagnosis method, and end-user, each offering insights into evolving patient needs and technological innovation.

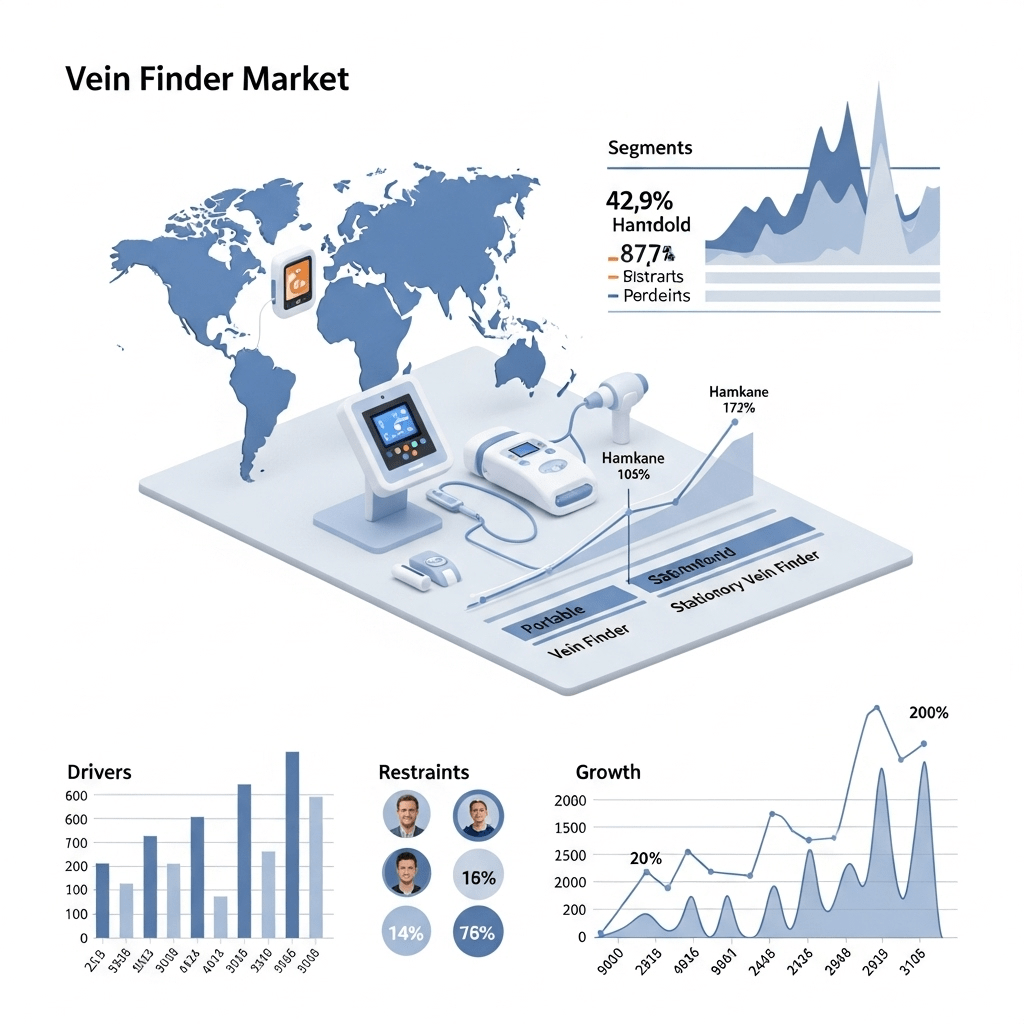

The vein finder market is valued at USD 38.78 million in 2025 and is slated to reach USD 54.18 million by 2035, which shows a CAGR of 3.4%. The increasing demand for non-invasive, accurate, and quick solutions for locating veins is driving market growth.

The vein finder market is experiencing robust growth driven by the increasing need for efficient vascular access in healthcare settings. Vein finder devices utilize advanced imaging technologies to improve vein visualization, significantly reducing failed attempts and patient discomfort during procedures like venipuncture, intravenous therapy, and blood draws. As hospitals and clinics prioritize patient safety and efficiency, the vein finder market has emerged as a vital component in modern medical practice.

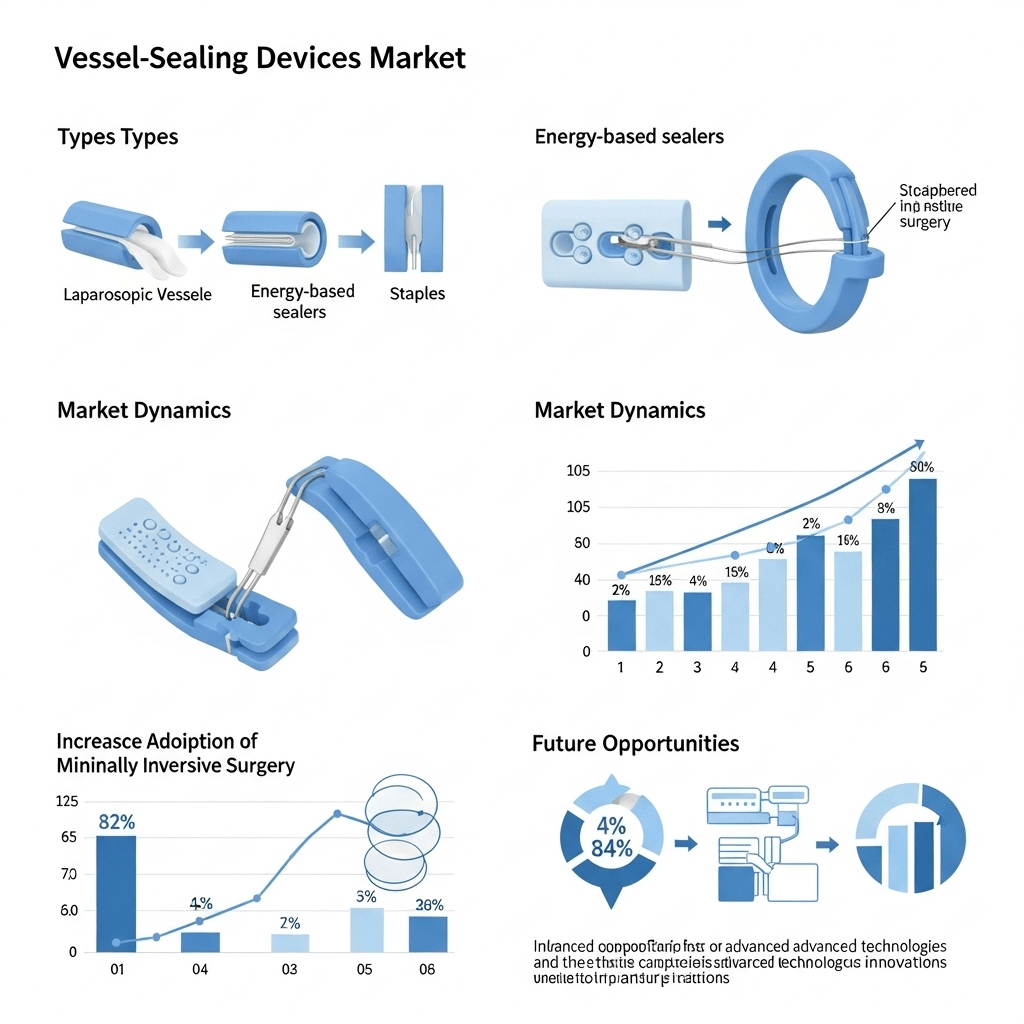

The global Vessel-sealing Devices Market is projected to be valued at USD 1,955.5 million in 2025 and is expected to reach USD 4,462.3 million by 2035, registering a CAGR of 8.6% during the forecast period, this growth is driven by the increasing demand for minimally invasive surgeries, advancements in energy-based sealing technologies, and the rising prevalence of chronic diseases necessitating surgical interventions.

The vessel-sealing devices market is evolving rapidly due to growing demand for minimally invasive surgical procedures and enhanced patient safety. These medical devices are critical for controlling bleeding by sealing blood vessels during surgeries. With technological advancements, the adoption of vessel-sealing systems in hospitals and ambulatory surgical centers is witnessing consistent growth.

Used widely in laparoscopic and open surgeries

Ensures effective hemostasis, reducing the risk of complications

Strong demand across general surgery, gynecology, and urology

The vessel-sealing devices market is supported by a combination of rising surgical volumes, innovation in electrosurgical technologies, and favorable reimbursement policies in developed countries. As healthcare systems continue to shift toward faster and more efficient surgical outcomes, the role of vessel-sealing equipment becomes increasingly important.

The vessel-sealing devices market is anticipated to show significant growth in the coming years, with increasing global healthcare expenditures and the prevalence of chronic diseases contributing to market expansion.

Estimated CAGR in the high single digits over the next five years

Market value expected to reach multi-billion USD range

Robotic-assisted surgeries boosting demand for advanced sealing systems

Integration with AI and smart sensors for precision sealing

Minimally invasive procedures are the key driver of the vessel-sealing devices market. This trend is supported by patient preference for less postoperative pain, shorter hospital stays, and faster recovery times.

Challenges and Opportunities

While the vessel-sealing devices market presents strong growth potential, it also faces several challenges that must be addressed to unlock future opportunities.

Challenges:

High cost of advanced vessel-sealing systems may limit accessibility

Stringent regulatory pathways can delay product launches

Limited adoption in low-income regions due to infrastructure gaps

Opportunities:

Expanding healthcare infrastructure in emerging markets

Technological advancements such as bipolar and ultrasonic sealing

Strategic collaborations and mergers among key players

Increasing demand for reusable and eco-friendly medical devices

Innovation in energy-based surgical tools and targeted R&D investment open new possibilities for expanding the vessel-sealing devices market, especially in outpatient and day-surgery environments.

Market Share by Geographical Region

The vessel-sealing devices market varies significantly across different regions, driven by healthcare spending, technological access, and demographic factors.

North America: Dominates the global vessel-sealing devices market due to advanced healthcare infrastructure, early technology adoption, and high surgical volumes.

Europe: Holds a substantial share, with Germany, France, and the UK leading in device usage and hospital innovation.

Asia-Pacific: Fastest-growing region with rising medical tourism, government healthcare initiatives, and growing investment in hospital equipment.

Latin America & Middle East: Steady growth driven by private healthcare expansion and increased surgeon training in modern surgical tools.

Geographic trends show that while North America and Europe lead in adoption, the Asia-Pacific region is rapidly catching up due to favorable government policies and a large patient population base.

Top Companies

Several key players are shaping the competitive landscape of the vessel-sealing devices market through innovation, acquisitions, and geographic expansion.

Medtronic: Offers a comprehensive range of vessel-sealing systems used in general and laparoscopic surgeries.

Johnson & Johnson (Ethicon): A leader in surgical innovation with a strong focus on energy-based instruments.

Olympus Corporation: Known for integrating advanced imaging with vessel-sealing capabilities.

B. Braun Melsungen AG: Offers reliable and cost-effective sealing solutions for hospitals worldwide.

Conmed Corporation: Expands market presence with advanced electrosurgical and laparoscopic tools.

These companies drive growth through strategic investments, robust R&D pipelines, and expansion into untapped markets, reinforcing their roles in the global vessel-sealing devices market.

The global sphingolipids market is projected to be valued at USD 693.9 million in 2025 and is expected to reach USD 1,145.6 million by 2035, registering a CAGR of 5.1% during the forecast period. This growth is driven by expanding applications in pharmaceuticals, nutraceuticals, and cosmetics.

The Sphingolipids Market has experienced notable expansion in recent years, driven by rising demand in the pharmaceutical, cosmetic, and food industries. Sphingolipids are a class of lipids that play vital roles in cell structure and signaling. Their therapeutic potential in managing chronic illnesses such as cancer, Alzheimer’s, and metabolic disorders has placed them at the forefront of biomedical research and commercial interest.

Key highlights of the market:

Increased research activities in lipidomics and molecular biology

Higher focus on disease-specific treatments involving sphingolipid pathways

Rising consumer demand for natural and bioactive ingredients in skincare

As innovation accelerates, the Sphingolipids Market is poised for sustained growth across diverse sectors.

The evolution of the Sphingolipids Market is shaped by several ongoing trends that indicate both expansion and transformation:

Increased use in dermatological products: Sphingolipids are being incorporated into moisturizers, anti-aging creams, and sunscreens due to their skin barrier-enhancing properties.

Functional food integration: Food and nutraceutical manufacturers are adding sphingolipids to enhance gut health and cognitive function.

Focus on bio-based synthesis: Companies are shifting toward plant- and yeast-derived sphingolipids to ensure sustainability and reduce production costs.

Technological advancements in extraction and analysis: Innovations in mass spectrometry and chromatography have enabled better characterization and utilization of sphingolipids.

These trends continue to drive the adaptability and relevance of the Sphingolipids Market in modern applications.

Driving Forces Behind Market Growth

Several powerful drivers are accelerating the expansion of the Sphingolipids Market, including:

Growing prevalence of chronic diseases: Increased cases of neurodegenerative and metabolic disorders are boosting demand for lipid-based therapeutic agents.

Expanding cosmetic industry: The rise in consumer awareness about skincare and anti-aging products has propelled the use of sphingolipids.

Personalized medicine advancements: As pharmaceutical companies develop targeted treatments, sphingolipids are being studied for their role in cell signaling and disease modulation.

Rising investments in biotech R&D: Government and private sector investments have intensified, supporting extensive lipidomics research.

The synergy of these factors is contributing to the steady rise of the Sphingolipids Market.

Challenges and Opportunities

Despite its promise, the Sphingolipids Market faces challenges that could impact its trajectory:

Key Challenges:

High production costs: Complex extraction and purification processes increase the cost of sphingolipid-based products.

Limited regulatory frameworks: The classification of sphingolipids across industries (food, pharma, cosmetics) can complicate compliance.

Lack of standardized methods: Varying research methodologies make it difficult to ensure consistent results and product efficacy.

Emerging Opportunities:

Growing demand in Asia-Pacific: Increasing health awareness and economic growth offer new consumer bases.

Collaborative research initiatives: Partnerships between academic institutions and private companies are fostering innovation.

Expansion into veterinary medicine: Applications in animal health represent an untapped market.

These hurdles and opportunities collectively shape the evolving landscape of the Sphingolipids Market.

Regional Analysis

Geographic insights into the Sphingolipids Market reveal dynamic regional performances:

North America: Dominates the global market due to strong R&D infrastructure and early adoption of new therapies.

Europe: Home to key biotech firms and supportive regulatory bodies focused on sustainable and natural products.

Asia-Pacific: Poised for rapid growth, driven by increasing investments, expanding pharmaceutical markets, and rising consumer awareness.

Latin America & MEA: Emerging regions showing gradual interest, with potential for long-term market penetration.

Regional diversity continues to define the global competitiveness of the Sphingolipids Market.

Top Companies

Several prominent players are making strategic moves in the Sphingolipids Market:

Avanti Polar Lipids, Inc.

Matreya LLC

Thermo Fisher Scientific Inc.

Merck KGaA

Evonik Industries AG

Tokyo Chemical Industry Co., Ltd.

Lipoid GmbH

These companies are involved in product innovation, strategic partnerships, and global expansion to enhance their market share.

The global Smart Pill Technologies is estimated to be valued at USD 900.3 million in 2025 and is projected to reach USD 1,855.5 million by 2035, registering a compound annual growth rate (CAGR) of 7.5% over the forecast period. The market is experiencing steady growth driven by rising demand for non-invasive gastrointestinal diagnostics, medication adherence monitoring, and precision drug delivery platforms.

The smart pill technologies market is revolutionizing the medical and healthcare industry by offering a futuristic approach to diagnosis, monitoring, and treatment. These ingestible devices contain sensors, imaging systems, and drug delivery mechanisms that can transmit data or perform actions within the human body. Unlike traditional pills, smart pill technologies combine medicine with micro-electronics to provide real-time feedback and improve patient outcomes.

Smart pill technologies are gaining widespread attention due to their potential to transform chronic disease management, early diagnosis, and personalized therapy. As healthcare shifts toward patient-centric solutions, the demand for these innovative tools continues to grow. Ingestible sensors, for instance, can monitor internal biological conditions and transmit information to external devices, making remote monitoring more effective.

Moreover, with the increasing prevalence of gastrointestinal disorders, diabetes, and cancer, healthcare providers and patients are looking for more efficient and less invasive diagnostic options. This shift is a key driver in the rising interest in smart pill technologies.

Market Trends

Increasing focus on personalized healthcare: Smart pill technologies enable targeted drug delivery and patient-specific diagnostics.

Growing adoption of digital health solutions: The integration of these pills with smartphones and cloud platforms allows continuous data monitoring.

Miniaturization of electronics: Technological advancements have made it feasible to fit sophisticated systems into a capsule-sized format.

Rising investment in biotech and medtech startups: Venture capital is pouring into companies developing next-gen smart pill technologies.

Increased awareness of preventive healthcare: Consumers are actively seeking tools that offer early detection and better disease management.

Challenges and Opportunities

Despite its promising potential, the smart pill technologies market faces several hurdles that must be addressed:

Regulatory complexity: Gaining approval from agencies like the FDA can be time-consuming and costly.

Data security concerns: Transmitting health data wirelessly presents privacy and cybersecurity challenges.

High development costs: The need for precision engineering and clinical testing makes smart pills expensive to produce.

Limited public awareness: Many patients are unfamiliar with the benefits and functions of these technologies.

Smart Pills Technologies Market

However, the opportunities are equally compelling:

Growing aging population: Older adults require frequent monitoring and chronic disease management, areas where smart pill technologies excel.

Expansion in telemedicine: Smart pills complement remote care models by offering real-time insights without in-person visits.

Partnerships between tech and healthcare firms: Collaborations are streamlining innovation and market entry.

Emerging markets: Countries in Asia-Pacific and Latin America are showing rising interest in adopting advanced healthcare solutions.

Key Points:

Smart pill technologies blend electronics and medicine for real-time diagnosis and treatment.

Chronic disease prevalence is driving demand for non-invasive, data-driven healthcare tools.

Regulatory approvals and high R&D costs remain primary challenges.

Technological progress and growing digital health trends are fueling market expansion.

Telemedicine and remote monitoring create a supportive ecosystem for smart pill adoption.

Key Regional Insights

North America: Leading the smart pill technologies market due to high healthcare spending, established regulatory frameworks, and active R&D.

Europe: Countries like Germany, the UK, and France are investing heavily in medical innovation and clinical trials for smart devices.

Asia-Pacific: Rapidly growing healthcare infrastructure and increasing awareness are creating opportunities in China, India, and Japan.

Latin America & Middle East: Although in the early adoption phase, improving digital infrastructure and public health policies are setting the stage for growth.

The global loop-mediated isothermal amplification (LAMP) market is projected to grow from USD 115.7 million in 2025 to USD 184.8 million by 2035, reflecting a compound annual growth rate (CAGR) of 4.9% during the forecast period. LAMP is an innovative nucleic acid amplification technique that offers rapid, cost-effective, and reliable diagnostics without the need for complex thermal cycling equipment. This simplicity makes it particularly advantageous for point-of-care testing and resource-limited settings.

The loop-mediated isothermal amplification market is gaining rapid traction due to its ability to deliver fast, accurate, and cost-effective molecular diagnostics. This technique, known as LAMP, allows DNA amplification under isothermal conditions, eliminating the need for expensive thermal cyclers. As healthcare systems around the world move toward point-of-care diagnostics, the loop-mediated isothermal amplification market is well-positioned to capitalize on this shift.

LAMP is widely used in infectious disease diagnosis, food safety, veterinary testing, and environmental monitoring.

The simplicity and speed of LAMP offer significant advantages over traditional PCR-based diagnostics.

As awareness grows in emerging economies, the loop-mediated isothermal amplification market continues to expand in both clinical and non-clinical applications.

The loop-mediated isothermal amplification market has shown consistent growth over the past few years, driven by an increasing demand for rapid diagnostics. The market is projected to grow steadily through 2030, with rising adoption in both developed and developing countries.

The market size reached a valuation of over USD 1 billion in recent years and is expected to continue its upward trajectory.

Growth is largely fueled by increased R&D investment and the need for efficient infectious disease testing, especially in low-resource settings.

Trends indicate a strong push toward portable LAMP testing kits, which can be used in rural and remote areas without access to centralized labs.

Loop-Mediated Isothermal Amplification Market

Challenges and Opportunities

While the loop-mediated isothermal amplification market offers significant benefits, it is not without challenges. However, these obstacles also open the door for innovation and new opportunities.

Challenges:

Lack of standardization in LAMP protocols across different diagnostic labs.

Limited public awareness and understanding of LAMP compared to PCR.

Regulatory barriers that may slow product approvals and global market entry.

Opportunities:

Growing interest in personalized medicine opens new applications for the loop-mediated isothermal amplification market.

Integration of LAMP with smartphone-based diagnostics and digital platforms.

Increasing demand for field-deployable diagnostic tools in agriculture and environmental testing.

Market Share by Geographical Region

The loop-mediated isothermal amplification market shows a distinct distribution pattern across various global regions. Each region contributes differently based on healthcare infrastructure, government policies, and demand for molecular diagnostics.

North America holds a significant share due to its advanced healthcare systems and high investment in molecular biology research.

Europe follows closely, supported by strong academic and industrial collaborations.

Asia-Pacific is emerging as a fast-growing region in the loop-mediated isothermal amplification market, thanks to large populations, improving healthcare access, and government-backed screening initiatives.

Latin America and Africa are still nascent markets, but increasing funding and health awareness are setting the stage for future growth.

Top Companies

Several major players dominate the loop-mediated isothermal amplification market. These companies are engaged in the development of innovative products and expanding their global presence.

Eiken Chemical Co., Ltd. – A pioneer in LAMP technology, offering robust testing kits for various applications.

New England Biolabs – Known for its extensive line of isothermal amplification reagents and solutions.

Meridian Bioscience, Inc. – Focuses on point-of-care diagnostics and LAMP-based molecular assays.

Lucira Health – Specializes in at-home molecular testing, offering compact LAMP-based solutions.

HiberGene Diagnostics – An emerging player gaining attention in hospital-based LAMP diagnostics.

These companies are investing heavily in R&D and regulatory compliance to enhance their product offerings and expand market penetration.

The loop-mediated isothermal amplification market can be segmented based on application, end-user, and product type. This segmentation helps identify the most lucrative areas for investment and strategic development.

The global Large Volume Wearable Injectors Market is estimated to be valued at USD 3,616.1 million in 2025 and is projected to reach USD 8,482.4 million by 2035, registering a compound annual growth rate (CAGR) of 8.9% over the forecast period. The market is experiencing accelerated growth driven by rising biologic drug volumes, increasing patient demand for home-based therapies, and payer-driven shifts toward outpatient drug delivery.

The Large Volume Wearable Injectors market is rapidly gaining momentum as healthcare shifts towards patient-centric, home-based solutions. These wearable drug delivery devices are engineered to administer high-volume biologics subcutaneously, offering convenience, improved compliance, and reduced hospital visits.

Designed for single-use or limited reuse, typically for chronic diseases like diabetes, cancer, and autoimmune disorders.

Devices can deliver doses over extended periods (from minutes to hours), enabling better pharmacokinetics.

They enhance quality of life by eliminating the need for intravenous administration in clinical settings.

Increasing prevalence of chronic illnesses drives demand for efficient, user-friendly drug delivery methods.

Trends within the Large Volume Wearable Injectors market indicate a dynamic shift in how patients receive treatments, supported by technological innovation and increasing regulatory approvals.

Growing interest in patient self-administration and home healthcare.

Rising R&D investment in biologics that require high-volume dosing.

Miniaturization and ergonomic design improvements in injector devices.

Expansion of connectivity features for remote monitoring and data tracking.

Increasing collaboration between pharmaceutical companies and device manufacturers.

Driving Forces Behind Market Growth

Multiple factors contribute to the expansion of the Large Volume Wearable Injectors market, making it one of the most promising segments in the drug delivery industry.

Rising chronic disease burden: Increasing incidence of diseases like cancer, rheumatoid arthritis, and diabetes fuels demand.

Biologic drug development: The surge in biologics needing large-volume delivery supports market growth.

Shift to outpatient care: Cost pressures and patient preference encourage treatment outside of hospitals.

Technological innovation: Smart sensors, Bluetooth connectivity, and automation enhance usability and effectiveness.

Regulatory support: Agencies like the FDA are streamlining approval processes for combination products, aiding faster market entry.

Challenges and Opportunities

Despite strong growth potential, the Large Volume Wearable Injectors market faces notable hurdles, though they are balanced by substantial opportunities.

High development costs: R&D and regulatory compliance require significant investment.

Patient adherence: Training and support are essential to ensure patients use devices correctly.

Opportunities:

Personalized medicine: Wearable injectors can be customized for individualized therapy.

Emerging markets: Untapped potential in Asia-Pacific, Latin America, and Africa.

Digital health integration: Combining drug delivery with health monitoring platforms presents new business models.

Regional Analysis

The growth trajectory of the Large Volume Wearable Injectors market varies by region, reflecting differences in healthcare infrastructure, regulatory frameworks, and disease prevalence.

North America: The largest market share due to advanced healthcare systems, strong biotech industry, and high adoption of innovative technologies.

Europe: Significant growth supported by public healthcare initiatives and aging populations.

Asia-Pacific: Fastest-growing region with rising chronic disease cases, expanding healthcare access, and increasing government support.

Latin America and Middle East & Africa: Gradual adoption with opportunities in improving healthcare delivery systems and affordability.

Top Companies

Several companies are leading the innovation and commercialization of Large Volume Wearable Injectors, shaping the competitive landscape.

Amgen Inc. – Known for its Onpro® kit, delivering Neulasta® in outpatient settings.

West Pharmaceutical Services, Inc. – Offers connected devices and integrated delivery platforms.

Ypsomed AG – Focuses on user-centric injector design and contract manufacturing.

Enable Injections – Specializes in large volume subcutaneous delivery systems.

BD (Becton, Dickinson and Company) – Provides a wide array of drug delivery technologies.

These companies are investing in partnerships, acquisitions, and product development to maintain their leadership.

The global inhalation contract development and manufacturing organization (CDMO) market is projected to grow from USD 9.13 billion in 2025 to USD 16.68 billion by 2035, reflecting a compound annual growth rate (CAGR) of 5.7% during the forecast period. This growth is driven by the increasing prevalence of respiratory diseases, advancements in inhalation drug delivery technologies, and the rising demand for outsourced manufacturing services in the pharmaceutical industry.

The inhalation CDMO market has emerged as a pivotal segment in the pharmaceutical contract development and manufacturing industry. With a rising demand for inhaled therapies for conditions like asthma, COPD, and cystic fibrosis, companies are increasingly outsourcing drug development and production to specialized partners. Inhalation CDMO services cater to both large pharmaceutical corporations and small biotech firms, offering expertise in formulation, device compatibility, regulatory support, and scale-up manufacturing.

This market is gaining traction due to the complexity of inhalation drug delivery, which often requires niche technical capabilities and specialized equipment. Outsourcing to an inhalation CDMO allows drug developers to reduce time-to-market while ensuring quality and compliance with global standards.

Several trends are shaping the growth trajectory of the inhalation CDMO market:

Rising prevalence of respiratory diseases such as asthma and chronic obstructive pulmonary disease (COPD), driving demand for effective inhalation therapies.

Increased adoption of dry powder inhalers (DPIs) and metered-dose inhalers (MDIs) as patient-friendly delivery systems.

Shift toward biologics and complex molecules delivered via inhalation, prompting investment in advanced CDMO technologies.

Growing importance of sustainability, with CDMOs focusing on eco-friendly propellants and packaging materials.

Expansion of digital health technologies, including smart inhalers integrated with sensors for monitoring patient adherence.

These trends are accelerating innovation in the inhalation CDMO market, prompting service providers to expand capabilities and enhance quality standards.

Challenges and Opportunities

The inhalation CDMO market faces certain roadblocks, but these also present opportunities for innovation and growth:

Challenges:

High development costs associated with inhalation drug-device combination products.

Regulatory complexity, especially in multi-region submissions involving stringent standards.

Limited availability of skilled personnel with expertise in inhalation formulation and device engineering.

Opportunities:

Rising demand for personalized medicine through inhalation routes offers niche market segments for CDMOs.

Partnerships and collaborations between pharma companies and CDMOs to accelerate clinical development.

Growth in emerging markets where respiratory diseases are on the rise, creating new client bases for CDMO services.

To stay competitive, companies must navigate these challenges while capitalizing on the expanding potential of the inhalation CDMO market.

Key Points:

The inhalation CDMO market is driven by increasing respiratory disease prevalence and growing demand for targeted drug delivery.

Outsourcing to CDMOs helps reduce time-to-market and supports compliance with evolving global regulations.

Innovation in smart inhalers and biologic formulations is opening new avenues for contract development services.

Regulatory expertise and device-engineering capabilities are essential differentiators for inhalation CDMOs.

Key Regional Insights

Geographically, the inhalation CDMO market exhibits distinct patterns of demand and development across regions:

North America holds a significant share due to advanced healthcare infrastructure, high R&D investment, and a strong presence of pharmaceutical giants.

Europe continues to grow steadily, supported by favorable reimbursement policies and demand for inhalation treatments in aging populations.

Asia-Pacific is emerging as a fast-growing region, with increased investment in healthcare infrastructure, rising incidence of respiratory conditions, and a growing number of local CDMOs.

Latin America and the Middle East & Africa show gradual growth, largely driven by improving access to healthcare and international partnerships with global pharma companies.

These regional dynamics are influencing investment patterns and strategic expansions in the inhalation CDMO market.

Top Companies

Several players dominate the inhalation CDMO market through technological expertise, global reach, and service portfolio diversity:

Lonza – Offers integrated inhalation solutions, including formulation, analytical development, and commercial manufacturing.

Catalent – Provides end-to-end inhalation services and device integration capabilities.

Recipharm – Known for its expertise in MDI and DPI development and filling.

Vectura – Specializes in inhalation development services with strong intellectual property and licensing options.

Hovione – Offers particle engineering and inhalation development, with a focus on dry powder inhalers.

Intertek – Provides regulatory and analytical support for inhaled product testing.

These companies are continually investing in facilities, talent, and technology to meet evolving customer needs in the inhalation CDMO market.