According to a recent market report titled “Oil and Gas Terminal Automation Market: Global Industry Analysis and Opportunity Assessment, 2016-2026” published by Future Market Insights, revenue from the global oil and gas terminal automation market is estimated to be valued at US$ 850 Mn in 2016. It is projected to exhibit 7.1% value CAGR during 2016-2026, and is forecast to be valued at US$ 1,693 Mn by 2026 end. The market is expected to witness nearly 2X growth between 2016 and 2026.

Growing need for liquefied natural gas, coupled with surplus oil and gas production in certain regions of the globe including North America has resulted in increasing focus on development of storage terminals across the globe. Accordingly, increase in investment towards development of oil and gas terminals is likely to be witnessed during forecast period. This, along with the existing demand-supply scenario is expected to boost revenue growth of the global oil and gas terminal automation market in the next 10 years. Growing emphasis on adoption of Wireless technology and Internet of Things (IoT) based terminal automation systems is anticipated to be witnessed during forecast period.

Get | Download Sample Copy with TOC, Graphs & List of Figures: https://www.futuremarketinsights.com/reports/sample/rep-gb-197

Growing concerns pertaining to cyber security and safety coupled with relatively higher initial capital investment associated with building a completely automated oil and gas terminal are likely to serve as impediments to growth of the global oil and gas terminal automation market between 2016 and 2026.

Segmentation highlights

Global oil and gas terminal automation market has been categorically divided into key market segments based on category and regions. On the basis of category, the market has been segmented into software, hardware, and services segments. These in turn are divided into key sub-segments.

- The Software category segment is projected to dominate the global oil and gas terminal automation market during the forecast period, accounting for a market share of nearly 38% in terms of value by the end of 2026. On the other hand, the hardware segment is estimated to witness 7.0% CAGR during forecast period to account for a market share of 33.7% in the overall oil and gas terminal automation market by 2026 end. Within the hardware segment, the HMI segment is likely to witness fast growth during 2016 –-2026.

Key Segments

On the basis of categories, the global oil and gas terminal automation market is segmented into:

Hardware

- ATG

- Blending Controllers

- SCADA

- PLC

- DCS

- HMI

- Safety; Security & Others

Software

- Terminal & Inventory Management

- Business System Integration

- Transaction Management

- Reporting

- Others

Services

- Commissioning

- Consulting Services

- Project Management

- Operations Services

- Training Services

Regional projections

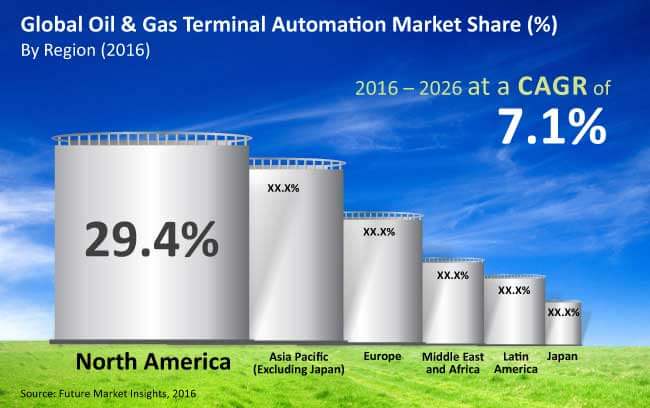

The North America and Asia Pacific excluding Japan (APEJ) markets are anticipated to emerge the dominant regional markets in the global oil and gas terminal automation market throughout the assessed period. Asia Pacific is estimated to project 8.8% CAGR in the forecast period, 2016–2026. The oil and gas terminal automation market in countries in Eastern Europe is also likely to witness steady growth in the next 10 years.

Vendor insights

The global oil and gas terminal automation market is dominated by a few top market companies such as Honeywell International Inc., Emerson Electric Co., ABB Group, Rockwell Automation, Inc., Yokogawa Electric Corporation, Siemens AG, FMC Technologies, Inc., and Schneider Electric SE. Certain key market companies are increasingly focussing on acquiring smaller players with specialised offerings – for instance, wireless technology based advanced systems – to better cater to the steadily growing global market demands so as to gain an edge over competition.

For More Information or Query or Customization Before Buying, Visit: https://www.futuremarketinsights.com/customization-available/rep-gb-197

About Industrial Automation Division at Future Market Insights

The Industrial Automation & Equipment division at FMI adopts a novel approach and innovative perspective in analyzing the global machinery and industrial automation market. A range of FMI’s market research reports offer comprehensive coverage of capital, portable, process, construction, industrial, and special purpose machinery used across manufacturing sector. The team also conducts distinctive analysis about installed base, consumables, replacement, and USP-feature application matrix, making us a prominent voice of authority in the industry. We are associates of choice for established as well as budding industry