According to recent market research by FMI, the global oil and gas hose assemblies market is projected to grow at a CAGR of 4.3% from 2023 to 2033. Valued at an estimated USD 1,409.5 million in 2023, the market is expected to reach USD 2,138.4 million by 2033. The growth is driven by increased investments in oil and gas projects worldwide, coupled with rising demand for high-pressure hose assemblies across sectors such as agriculture, chemicals, and energy.

Oil and Gas Hose Assemblies Market – Key Highlights

North America accounts for the majority of market share as a result of the presence of leading players and growing investments in the oil & gas ventures.

Midstream application type to foresee a surge in demand during the forecast period.

High-pressure intake category is anticipated to expand at a notable CAGR during 2020-2030.

Polymers and composites remain majorly preferred among other material types.

Dock and hose assemblies to remain key beneficiary among other product category.

Oil and Gas Hose Assemblies Market – Drivers

Growing demand for downstream applications to spur overall market growth.

Increasing innovations in raw materials of hoes providing lucrative prospects throughout the forecast period.

Novel subsea technologies are the foremost contributor to the expansion of the market.

Oil and Gas Hose Assemblies Market – Restraints

Lack of skilled workers with the technical proficiency of oil & gas hoses is the key challenge for the market.

Less focus of manufacturers on technological advancements and the accessibility of few manufacturing raw materials are limiting growth.

COVID-19 Impact on the Market

The COVID-19 outbreak has negatively impacted several different sectors, comprising the oil & gas hose assemblies market. The lockdown has led to closures of manufacturing plants, limiting sales in the market. The market is anticipated to incur a -7.2% decline in valuation during 2020. However, as per the market analysis, the market will recover from 2021 onwards, and then growing at a sturdy pace towards 2030 end.

Competitive Landscape

Major companies operating in the global market include Eaton Corporation Plc, Gates Corporation, Continental AG, ERIKS North America, Inc. Trelleborg AB, ParkerHannifin Corporation, ALFA GOMMA Spa, Manuli Hydraulics, and Kuriyama Holdings Corporation.

Key Segments

Product Type:

Dock LoadingHose Assemblies

Dump HoseAssemblies

FPSO WaterUptake Hoses

Jumper HoseAssemblies

Bunkering HoseAssemblies

Drilling MudHose Assemblies

Frac HoseAssemblies

Other CustomHose Assemblies

Material Type:

Rubber

Polymers & Composites

Metal

Application Type:

Downstream

Midstream

Upstream

Pressure Intake:

Low Pressure

Medium Pressure

High Pressure

Regional Outlook:

North America – United States, Canada

Latin America – Brazil, Mexico, and the rest of Latin America

Europe – Germany, France, Italy, United Kingdom, Spain, Russia, and the rest of Europe

South Asia and Pacific – India, ASEAN, Australia, and New Zealand, and the rest of South Asia and Pacific

East Asia – China, Japan, and South Korea

Middle East & Africa – GCC counties, North Africa, South Africa, Türkiye, and the rest of Middle East And Africa

Future Market Insights, Inc. (ESOMAR certified, recipient of the Stevie Award, and a member of the Greater New York Chamber of Commerce) offers profound insights into the driving factors that are boosting demand in the market. FMI stands as the leading global provider of market intelligence, advisory services, consulting, and events for the Packaging, Food and Beverage, Consumer Technology, Healthcare, Industrial, and Chemicals markets. With a vast team of over 400 analysts worldwide, FMI provides global, regional, and local expertise on diverse domains and industry trends across more than 110 countries.

The Soft Touch Polyurethane Coatings market is experiencing significant growth as demand for high-quality, tactile, and durable finishes in automotive, furniture, and consumer electronics industries continues to rise. These coatings, known for their velvety texture and excellent abrasion resistance, have gained popularity due to their ability to provide enhanced aesthetics and improved functionality to a range of surfaces.

The global soft touch polyurethane coatings industry is expected to reach a value of USD 17,429 million by 2033, growing at a robust CAGR of 9% from 2023 to 2033. This growth is driven by the increasing demand for coatings that provide superior tactile properties, durability, and aesthetic appeal, particularly in automotive, furniture, and consumer electronics applications. As industries seek coatings that enhance product quality and consumer experience, the soft touch polyurethane coatings market is poised for significant expansion in the coming decade.

Market Overview:

Soft Touch Polyurethane Coatings are widely used to impart a smooth, rubber-like finish to products. Their applications extend across automotive interiors, consumer electronics, furniture, packaging, and more. These coatings are primarily recognized for their durability, ease of maintenance, and enhanced feel, making them ideal for consumer products requiring a premium look and feel.

Market Growth Drivers:

Several factors contribute to the rapid growth of the Soft Touch Polyurethane Coatings market:

Increasing Demand for Premium Products: The rise in disposable income and shifting consumer preferences towards high-end, premium quality goods, particularly in automotive interiors and electronics, has fueled the demand for soft-touch finishes.

Automotive Industry Expansion: As the automotive industry continues to innovate, there is a rising demand for coatings that provide both aesthetic appeal and long-lasting protection for interior and exterior components.

Consumer Electronics Growth: With the rise of smartphones, tablets, and other electronics, manufacturers seek materials that enhance the tactile experience of users. Soft Touch Polyurethane Coatings provide an appealing solution, making them widely adopted for device exteriors and accessories.

Furniture and Home Décor: The growing trend for sleek, modern furniture and home décor items has also increased demand for coatings that offer durability and a soft, pleasant touch, particularly in high-end products.

Sustainability and Eco-friendly Trends: There is a growing trend toward sustainable production processes. Soft Touch Polyurethane Coatings manufacturers are focusing on developing environmentally friendly formulations, which are gaining popularity in a wide range of industries.

Trends and Opportunities:

Technological Advancements: Ongoing advancements in coating formulations are expected to enhance the performance of Soft Touch Polyurethane Coatings. This includes better UV resistance, improved scratch resistance, and lower environmental impact, opening new avenues for growth.

Customization and Versatility: The ability to customize Soft Touch Polyurethane Coatings for specific applications, including various textures and colors, is a key trend. This versatility makes them highly desirable across multiple industries, providing opportunities for product differentiation.

Growing Urbanization and Changing Lifestyles: As urbanization and changing consumer lifestyles drive demand for more stylish and functional consumer goods, the market for Soft Touch Polyurethane Coatings is expected to expand, particularly in regions with a growing middle-class population.

Leading Players in the Soft Touch Polyurethane Coatings Market

RPM International Inc.

The Sherwin Williams Company

PPG Industries Inc.

Axalta Coating Systems Ltd.

Jotun AS

AkzoNobel N.V.

Aexcel Corporation

Sokan New Materials.

Huntsman International LLC

DuPont

Regional Analysis:

North America: The North American market is one of the largest and fastest-growing regions, driven by the automotive and consumer electronics industries. Increased investment in research and development by major coating manufacturers is expected to fuel further growth in this region.

Europe: Europe is a key market for Soft Touch Polyurethane Coatings, particularly in the automotive, furniture, and consumer electronics sectors. The region’s emphasis on luxury products and eco-friendly solutions will continue to propel market growth.

Asia-Pacific: The Asia-Pacific region is expected to witness the highest growth rate, driven by rapid industrialization, urbanization, and a growing demand for consumer electronics and automobiles. Countries like China, India, and Japan are leading the way with increasing adoption of high-quality finishes in their products.

Latin America and the Middle East & Africa: Emerging markets in Latin America and the Middle East & Africa are anticipated to grow steadily as economic conditions improve and consumer demand for high-end products rises. This offers significant opportunities for market expansion.

About Future Market Insights (FMI)

Future Market Insights, Inc. (ESOMAR certified, recipient of the Stevie Award, and a member of the Greater New York Chamber of Commerce) offers profound insights into the driving factors that are boosting demand in the market. FMI stands as the leading global provider of market intelligence, advisory services, consulting, and events for the Packaging, Food and Beverage, Consumer Technology, Healthcare, Industrial, and Chemicals markets. With a vast team of over 400 analystsworldwide, FMI provides global, regional, and local expertise on diverse domains and industry trends across more than 110 countries. Join us as we commemorate 10 years of delivering trusted market insights. Reflecting on a decade of achievements, we continue to lead with integrity, innovation, and expertise.

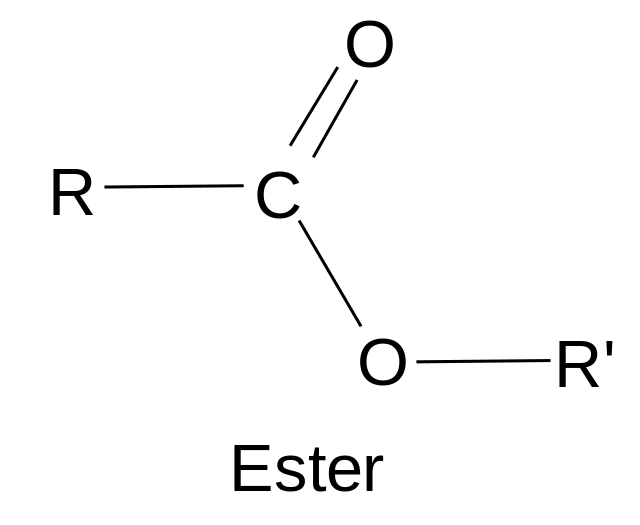

The global esters market is experiencing significant growth, driven by diverse applications across industries such as chemicals, pharmaceuticals, cosmetics, and food & beverages. Esters, organic compounds formed by the reaction of acids and alcohols, are highly valued for their versatility in both industrial and consumer applications. As the demand for eco-friendly and cost-effective solutions grows, the esters market is expected to expand at a robust pace in the coming years.

The global esters market is projected to grow at a CAGR of 5.4%, reaching a value of USD 159.36 billion by 2033. This growth is fueled by the increasing demand for esters in various industries, including automotive, pharmaceuticals, and food processing, due to their versatile applications and favorable properties.

Market Growth Drivers

Industrial Applications: The growth of various end-use industries such as automotive, construction, and textiles is a key driver for the esters market. Esters are essential in the manufacturing of lubricants, paints, and coatings, owing to their excellent solubility and low toxicity.

Pharmaceuticals and Cosmetics: The pharmaceutical sector’s increasing demand for high-quality ester-based products, such as active pharmaceutical ingredients (APIs) and solubilizers, is propelling market growth. Similarly, esters are widely used in cosmetics and personal care products due to their ability to enhance fragrances and improve product texture.

Sustainability Focus: As industries and consumers increasingly focus on sustainability, the demand for bio-based esters made from renewable resources is rising. This trend is particularly evident in the food and beverage sector, where esters are used as flavorings, preservatives, and fragrances.

Expanding Food and Beverage Applications: Esters are extensively used in the food industry for their ability to impart fruity flavors and as preservatives. The growing popularity of processed foods and beverages, particularly in emerging economies, is a significant market driver.

Rising Demand for Personal Care Products: Esters’ role as emollients, emulsifiers, and surfactants in personal care and cosmetic products, including skin care and hair care formulations, continues to rise as consumers become more aware of their benefits.

Key Trends in the Esters Market

Bio-Based Esters: There is a noticeable shift toward bio-based esters due to increasing consumer demand for environmentally-friendly and sustainable alternatives. This is expected to be one of the dominant trends, particularly in the food, personal care, and automotive sectors.

Product Innovation: The market is witnessing substantial product innovation as manufacturers develop new types of esters with enhanced properties. Custom formulations are being tailored to meet the specific needs of industries such as pharmaceuticals, cosmetics, and agriculture.

Regulatory Pressure for Green Chemistry: The implementation of stringent environmental regulations has pushed manufacturers to adopt green chemistry principles. This includes the development of eco-friendly esters that are biodegradable and have a minimal environmental footprint.

Consolidation and Mergers: The esters market is experiencing consolidation, with major players merging or acquiring smaller competitors to expand their market reach and improve product portfolios.

Opportunities in the Esters Market

Emerging Economies: The demand for esters in emerging economies, particularly in Asia-Pacific and Latin America, is expected to surge as these regions see a rise in industrial activities, consumer goods production, and urbanization.

Technological Advancements: Innovation in ester production technology, including the development of more efficient catalytic processes and advanced esterification techniques, is expected to lower production costs and enhance product yields, opening up new growth opportunities.

Growth in the Automotive and Electronics Sectors: Esters are used in lubricants and coatings within the automotive and electronics industries. As these sectors continue to expand globally, particularly with the rise of electric vehicles and advanced manufacturing technologies, the demand for ester-based products is set to increase.

Future Market Insights, Inc. (ESOMAR certified, recipient of the Stevie Award, and a member of the Greater New York Chamber of Commerce) offers profound insights into the driving factors that are boosting demand in the market. FMI stands as the leading global provider of market intelligence, advisory services, consulting, and events for the Packaging, Food and Beverage, Consumer Technology, Healthcare, Industrial, and Chemicals markets. With a vast team of over 400 analystsworldwide, FMI provides global, regional, and local expertise on diverse domains and industry trends across more than 110 countries. Join us as we commemorate 10 years of delivering trusted market insights. Reflecting on a decade of achievements, we continue to lead with integrity, innovation, and expertise.

The global mining flotation chemicals market is poised for significant growth in the coming years, driven by the rising demand for minerals in various industries, advancements in mining technologies, and the growing need for efficient and eco-friendly chemical solutions. As key players in the mining and mineral processing industries continue to invest in innovation, the market for flotation chemicals is projected to expand at a substantial rate.

The global mining flotation chemicals market is expected to grow at a healthy CAGR of 5%, reaching a value of USD 19,360.2 million by 2033. This growth is driven by increasing demand for mining chemicals in the extraction and processing of minerals.

Understanding the Mining Flotation Chemicals Market

Mining flotation chemicals are substances used in the flotation process to separate valuable minerals from ores during the mineral processing stage. These chemicals play a pivotal role in improving the efficiency of the flotation process, which is crucial for extracting valuable minerals such as copper, gold, silver, and other metals. The chemicals are typically categorized into collectors, frothers, modifiers, and dispersants, each serving a specific function in the flotation process.

Market Growth Drivers

Increasing Demand for Minerals: As global industrialization continues, there is a surge in demand for critical minerals like copper, lithium, and gold, essential for industries ranging from construction to electronics. This demand is directly contributing to the increased adoption of flotation chemicals in the mining industry.

Technological Advancements: The continuous development of new flotation chemical formulations and mining technologies is enhancing the efficiency of mineral extraction processes. Innovations aimed at improving recovery rates and reducing energy consumption are driving the market.

Environmental Regulations: The growing focus on sustainable mining practices and the implementation of stricter environmental regulations have led to a shift towards more eco-friendly flotation chemicals. Companies are increasingly adopting chemicals that are less toxic and have a minimal environmental footprint.

Emerging Economies: The expansion of mining activities in emerging economies, particularly in regions like Africa, Asia, and Latin America, is expected to boost the demand for flotation chemicals. These regions are rich in untapped mineral resources, which require effective flotation processes for extraction.

Trends and Opportunities

Eco-friendly Flotation Chemicals: There is a noticeable trend toward the development of bio-based and environmentally safe flotation chemicals. These chemicals are gaining traction as mining companies seek to minimize their environmental impact while ensuring high efficiency in mineral recovery.

Automation and Digitalization in Mining: The mining industry is embracing automation and digital technologies to optimize operations. The integration of sensors and AI-driven systems to monitor and control flotation processes is creating opportunities for more precise and efficient chemical usage.

Diversification of End-User Applications: While the primary end-users of flotation chemicals are in the metal mining sector, there is growing demand from other industries, such as coal and industrial minerals. This diversification offers new revenue streams for flotation chemical manufacturers.

Strategic Partnerships and Mergers: The mining flotation chemicals market is witnessing an increase in strategic collaborations, partnerships, and mergers between chemical suppliers and mining companies. These partnerships are focused on improving product offerings and expanding regional footprints.

North America: The mining flotation chemicals market in North America is expected to witness steady growth due to the region’s established mining industry, especially in countries like the United States and Canada. The growing demand for lithium and copper, coupled with the adoption of advanced flotation technologies, will drive market growth.

Asia-Pacific: Asia-Pacific holds a dominant position in the global market, driven by large-scale mining activities in countries like China, India, and Australia. China, in particular, is a major consumer of flotation chemicals due to its vast mining operations and demand for a variety of minerals.

Europe: Europe is focusing on increasing its mining capabilities, particularly in countries such as Russia and Sweden, which are rich in mineral resources. The push towards more sustainable mining practices is expected to fuel the demand for environmentally friendly flotation chemicals.

Latin America: Latin America is witnessing a surge in mining operations, particularly in Brazil, Chile, and Peru, which are known for their rich mineral deposits. As the demand for copper and lithium grows, so does the need for flotation chemicals, positioning the region as a key growth area.

Middle East & Africa: The Middle East and Africa are emerging as significant players in the mining industry. With abundant untapped mineral resources, the demand for flotation chemicals is expected to increase, particularly in countries like South Africa and Morocco.

About Future Market Insights (FMI)

Future Market Insights, Inc. (ESOMAR certified, recipient of the Stevie Award, and a member of the Greater New York Chamber of Commerce) offers profound insights into the driving factors that are boosting demand in the market. FMI stands as the leading global provider of market intelligence, advisory services, consulting, and events for the Packaging, Food and Beverage, Consumer Technology, Healthcare, Industrial, and Chemicals markets. With a vast team of over 400 analystsworldwide, FMI provides global, regional, and local expertise on diverse domains and industry trends across more than 110 countries. Join us as we commemorate 10 years of delivering trusted market insights. Reflecting on a decade of achievements, we continue to lead with integrity, innovation, and expertise.

The pearlescent pigment market is set to witness steady growth, with a projected compound annual growth rate (CAGR) of 4% during the forecast period, ultimately exceeding a market value of USD 5,544.7 million by 2033. This growth is primarily driven by the increasing demand for visually appealing, high-quality pigments across various industries, including automotive, cosmetics, paints and coatings, and packaging. The rising popularity of pearlescent effects in consumer products, coupled with the growing trend of innovative designs and aesthetic appeal, is expected to propel the demand for these pigments. Additionally, the market will benefit from advancements in production technologies and the expansion of applications in high-end and luxury goods.

Manufacturers of automotive and industrial coatings are opting for pearlescent pigment for their aesthetic brilliance and exclusivity, thus enhancing the look of their products. Additionally, efficacious, special-effect pearl pigments enhance the sustainability quotient of the final product due to their inherent sustainability.

Sustainable pearlescent pigments have low VOC volume and better performance attributes like durability, better barrier resistance, and thermal stability. Since customers are becoming discerning of the potential environmental damage, they are increasingly considering options that allow them to reduce their overall carbon footprint. Based on these factors, the market is expected to expand over the forecast period.

This pigment has also stepped foot in the personal care and cosmetics industry, and since its arrival, it has revolutionized how consumers perceive beauty and appearance. This is credited to its cost-effectiveness, which makes achieving a ‘celebrity’ look possible on a budget. Many powders, creams, and lotions for personal care consist of natural pearl essence as an eco-friendly, dermatologically tested substitute to its toxic and synthetic counterparts.

Key consumers for this pigment are India, China, and Brazil due to their adoption quotient and surging per capita income. Moreover, the popularization of mass-customized goods and surging governmental assistance is expected to push construction activities and automotive production, thus broadening the application scope of these pigments.

Top Highlights from the FMI’s Analysis of the Pearlescent Pigment Market:

As per FMI estimates, the United States’ stake in the global market is 27.3%, making it an ideal candidate for future business prospects.

Germany is expected to enjoy a market share of 6.8% in 2023, suggesting considerable opportunities for growth.

Australia is expected to attain 5.9%, representing one of the core markets for pearlescent pigment. Manufacturers are projected to explore burgeoning prospects in the country.

Japan’s share is estimated to be 5.6%, demonstrating a substantial market for business ventures of pearlescent pigment.

India is expected to expand at a CAGR of 4.8% over the forecast period, suggesting more investments are underway by manufacturers.

China and the United Kingdom are anticipated to expand at CAGRs of 4.4% and 3.9%, respectively, over the forecast period.

Based on purity type, natural pearl pigment is expected to take up the majority of the market share by gaining 67.4% in 2023.

Based on end use industry, the automotive paints industry is expected to contribute 39.3% market share in 2023.

Market Developments Shaping the Pearlescent Pigment Industry

Sun Chemical introduced Xennia Pearl pigment inks in October 2021. The latter is used in fast-paced industrial applications. This consists of inks for both mid and high-viscosity printheads. The firm stated the creation of this product for its multi-substrate compatibility, robustness, consistent color, and excellent print performance.

DIC Corporation and Sun Chemical, its subsidiary firm, obtained Seller Ink in September 2020. The latter company is a Brazil-based producer of specialty inks and coatings. This acquisition is expected to help Sun Chemical expand its specialty inks and coatings business in Latin America.

BASF SE released eXpand! Blue EH 6001 in March 2019. The product is marketed under its brand name Colours & Effects. This product came to fruition due to a partnership between Landa Labs and BASF.

Fujian Kuncai Fine Chemicals Co. Ltd. introduced the “Dove Grey” pigment in May 2019. This pigment is a semi-transparent neutral grey hue, used mainly for industrial applications.

Shanghai Zhuerna High-Tech Powder Material Co., Ltd

Oxen Special Chemicals Co., Ltd

Huaian Concord Industrial Product Co., Ltd.

Spectra Colours Ltd

LANSCO COLORS

Aal Chem

Zhejiang Ruicheng Effect Pigment Co., Ltd

Sinpearl Pearlescent Pigment Co., Ltd

Kolorjet Chemicals Pvt Ltd

About Future Market Insights (FMI)

Future Market Insights, Inc. (ESOMAR certified, recipient of the Stevie Award, and a member of the Greater New York Chamber of Commerce) offers profound insights into the driving factors that are boosting demand in the market. FMI stands as the leading global provider of market intelligence, advisory services, consulting, and events for the Packaging, Food and Beverage, Consumer Technology, Healthcare, Industrial, and Chemicals markets. With a vast team of over 400 analystsworldwide, FMI provides global, regional, and local expertise on diverse domains and industry trends across more than 110 countries. Join us as we commemorate 10 years of delivering trusted market insights. Reflecting on a decade of achievements, we continue to lead with integrity, innovation, and expertise.

The global alumina trihydrate (ATH) market is set to experience robust growth, with a remarkable compound annual growth rate (CAGR) of 7.7% from 2023 to 2033. This expansion is driven by increasing demand for ATH in various applications such as flame retardants, water treatment, and as a filler in the construction and automotive industries. ATH’s eco-friendly properties and growing use in fire-resistant materials, particularly in the manufacturing of plastics, paints, and coatings, further contribute to its market growth. By 2033, the global ATH market is expected to surpass a valuation of USD 11,180.1 million, reflecting its crucial role in advancing sustainable and fire-safe technologies across multiple sectors.

The growth of the global alumina trihydrate market is attributed to its diverse application in numerous industries such as plastics, papers, paints & coatings, and others is the key factor propelling the growth. All these industries rely heavily on alumina trihydrate, and their anticipated expansion should fuel aluminum hydroxide sales. It has been estimated that more than 90% of alumina trihydrate production goes into manufacturing aluminum. When alumina trihydrate is used for flame retardant applications, it suppresses and reduces fire spread via plastic.

Alumina trihydrate or aluminum hydroxide is known for its power source from bauxite. It is translucent and white in color. Through exposure to heat, alumina trihydrate converts to aluminum oxide and releases water. The powder is most commonly used for preparing transparent lake pigments.

The Alumina Trihydrate (ATH) market is witnessing notable growth and several trends and opportunities, driven by its wide range of applications in various industries such as construction, automotive, and pharmaceuticals. Here are some key trends and opportunities in the ATH market:

1. Increasing Demand for Flame Retardants

ATH is a key component in flame retardant formulations, particularly in plastics, rubber, and textiles. As fire safety regulations tighten across industries, especially in construction, automotive, and electronics, the demand for ATH-based flame retardants is expected to rise. ATH serves as a non-toxic and cost-effective alternative to other flame retardants, making it an attractive choice for manufacturers.

2. Growth in the Construction and Building Industry

ATH is used in the production of cement and as a filler in paints and coatings, where it improves durability and enhances fire resistance. The rapid urbanization and growing construction activities in emerging economies, especially in Asia-Pacific, present significant opportunities for ATH producers. The increasing focus on sustainable construction materials further promotes the demand for ATH due to its eco-friendly properties.

3. Advances in Electric Vehicles (EV) and Automotive Industry

As the automotive industry shifts towards electric vehicles (EVs), ATH finds use in the production of components such as batteries, cables, and circuit boards. The growing demand for lightweight, durable, and fire-resistant materials in EVs creates new opportunities for ATH suppliers. The increasing adoption of ATH-based materials in automotive manufacturing will likely support market expansion.

4. Applications in Water Treatment

ATH is also used in water treatment processes as a flocculant and coagulant, especially for removing impurities like suspended solids and heavy metals from water. As global water scarcity and pollution concerns intensify, the demand for water purification solutions is growing. This trend provides a substantial opportunity for ATH in the environmental sector.

5. Growing Demand in Pharmaceuticals and Cosmetics

ATH is utilized as an excipient in the pharmaceutical industry, particularly in the production of tablets and as a stabilizer in liquid formulations. Additionally, ATH is used in cosmetics for its properties as a mild abrasive and in skin care products. The growing pharmaceutical and personal care sectors present a steady demand for ATH in these applications.

Report Highlights

Alumina trihydrate comprises antacid properties and can facilitate the maintenance of optimum pH in the gastrointestinal tract. Its antacid properties are likely to make aluminum hydroxide demand soar from the worldwide pharmaceuticals industry. Furthermore, its excellent filler qualities make it suitable for use in plastics, cosmetics, detergents, inks, ceramics, and glass. It is also an excellent water-repellent, flame-retardant, and paper coating.

Over recent years, strict fire safety regulations have come into force all over the world. This has resulted in augmenting demand for high-quality flame retardants that have been on a consistent rise. Future Market Insights (FMI) expects this trend to continue between 2023 and 2033.

Throughout the assessment period, non-halogenated flame retardant demand elevated all over the globe, owing to various fire-related accidents. The use of alumina trihydrate also gained traction for engineering papers, plastics, rubbers, paints, and coatings. Automobiles with low weights tend to be more fuel efficient as it takes less power to move them compared to heavy all-metal vehicles.

Recent Developments

Approximately 10 to 15% of any modern-day vehicle’s weight includes plastic composites. Owing to these factors, automobile manufacturers are increasingly preferring these composites over metals. The use of metals can add to the strength and durability of automobiles.

Other kinds of metals also tend to make vehicles heavy, which is likely to impact their fuel economies adversely. Plastic composites engineered using alumina trihydrate can reduce a vehicle’s weight significantly. Among several car owners all over the globe, fuel economy has become a prominent talking point.

Fuel prices have been steadily rising in recent years, and vehicle owners are on the lookout for products that offer fuel economy benefits. Moreover, FMI anticipates this trend to persist over the next decade and drive alumina trihydrate demand. Using alumina trihydrate in automobile manufacturing as an alternative to titanium dioxide can also lower production costs by around 25%.

Attributing to the widespread expansion of the alumina trihydrate market, the competition is predicted to grow fiercer due to the presence of dominant regional and international players in the market. The market still has a fair way to go before it reaches a saturation point. FMI anticipates both leading and emerging players to expand production facilities based on trends from the recent past.

There are massive investments in research and development activities as manufacturers are keen on reducing costs and improving quality. Acquisitions and mergers look probable too.

In January 2023, ChemIndia, a company based in India, announced the launch of extender pigment products which include alumina hydrate. In August 2022, Cimbar Resources Inc. acquired the manufacturing assets of Imerys Carbonates USA Inc. related to calcium carbonate manufacturing.

Top Key Players in the Alumina Trihydrate Market

Sumitomo Chemical Co. Ltd.

Aluminum Corp. of China Ltd.

Nabaltec AG

National Aluminium Company Ltd.

Huber Engineered Materials

SCR Sibelco NV

R.J. Marshall Company

Alteo

Southern Ionics Incorporated

ALUMINA CHEMICALS and CASTABLES

About Future Market Insights (FMI)

Future Market Insights, Inc. (ESOMAR certified, recipient of the Stevie Award, and a member of the Greater New York Chamber of Commerce) offers profound insights into the driving factors that are boosting demand in the market. FMI stands as the leading global provider of market intelligence, advisory services, consulting, and events for the Packaging, Food and Beverage, Consumer Technology, Healthcare, Industrial, and Chemicals markets. With a vast team of over 400 analystsworldwide, FMI provides global, regional, and local expertise on diverse domains and industry trends across more than 110 countries. Join us as we commemorate 10 years of delivering trusted market insights. Reflecting on a decade of achievements, we continue to lead with integrity, innovation, and expertise.

The global sulfur-coated urea market is projected to grow at a steady CAGR of 3.3%, reaching a valuation of over USD 1,453 million by 2032. This growth is largely driven by sulfur’s diverse applications across various industries, notably in agriculture, golf courses, professional lawn care, turf management, and greenhouse cultivation. In agriculture, sulfur-coated urea is increasingly preferred for its efficiency in providing a slow-release nitrogen source, promoting healthy plant growth while minimizing nutrient loss. Additionally, the rising demand for well-maintained green spaces and professional landscaping services has bolstered the adoption of sulfur-coated urea in turf and lawn care sectors, further supporting market expansion.

The increased availability of several other coated particles which resulted in stagnant market growth across the forecast period from 2022 to 2032 is expected to propel the demand for Sulphur coated urea market. In addition to that, the market is expected to excel amid a surging number of golf courses globally and increased spending on luxury amenities such as household lawns.

Sulfur-Coated Urea Market Growth Drivers

Increased Agricultural Demand: Sulfur-coated urea is increasingly favored in agriculture due to its slow-release nitrogen properties, which enhance crop yield and reduce nutrient loss, making it a sustainable choice for farmers worldwide.

Advancements in Fertilizer Technology: The development of more efficient sulfur-coated urea formulations, which optimize nutrient delivery and minimize environmental impact, is fueling its adoption in both conventional and organic farming practices.

Rising Need for Sustainable Agricultural Practices: With the global push towards more eco-friendly and sustainable farming, sulfur-coated urea offers an ideal solution, reducing fertilizer application frequency and minimizing the risk of leaching and volatilization.

Growing Demand in Turf and Lawn Care: The use of sulfur-coated urea in professional lawn care, golf courses, and turf management is expanding due to its ability to promote healthy, green growth over extended periods, making it a preferred choice in landscaping.

Expansion of Greenhouse and Horticultural Practices: The rise of greenhouse farming and controlled environment agriculture has led to a surge in the use of sulfur-coated urea, as it provides consistent nutrient supply for plants in these specialized growing conditions.

Government Support for Fertilizer Use: Government initiatives to improve agricultural productivity and efficiency, along with subsidies and favorable policies, are promoting the widespread adoption of advanced fertilizer products like sulfur-coated urea.

Environmental Concerns and Fertilizer Efficiency: As environmental concerns over fertilizer runoff grow, sulfur-coated urea’s slow-release technology helps address these issues, reducing environmental harm while increasing fertilizer use efficiency.

Dominant players in the market are focused on heavy investments and innovations for the development of products with improved applications and the introduction of sustainable products in order to minimize carbon footprints. On the other hand, some of the other players are concentrating on capacity expansions in emerging economies to capitalize on expanding their agriculture sector.

Key Companies Profiled

Nutrien Ltd.; J.R. Simplot Chemicals; Turf Care Supply, LLC; Israel Chemicals Ltd.; The Andersons, Inc.; Everris; Syngenta AG; Hanfeng Evergreen; Yara International ASA; Haifa Chemicals Ltd.; Koch Industries Inc.; Luyue Chemical; Luxi Chemical; Harrell’s LLC; PULCU TARIM; QAFCO; Others

More Insights into the Sulphur Coated Urea Market

According to FMI estimations, the U.S. is expected to remain one of the leading consumers of Sulphur coated urea attributing to the rising applications in diverse industries including the residential sector and the agriculture sector among others. The country is predicted to account for about 20%-25% of the global value share in the Sulphur coated urea market.

Emerging economies like China, Japan, and Australia are expected to be the fastest growing Sulphur coated urea market all over the Asia Pacific region owing to the rising preference for luxury amenities such as golf courses, community shades, horticulture, gardens, etc., which is creating a conducive environment for key players in the region.

About Future Market Insights (FMI)

Future Market Insights, Inc. (ESOMAR certified, recipient of the Stevie Award, and a member of the Greater New York Chamber of Commerce) offers profound insights into the driving factors that are boosting demand in the market. FMI stands as the leading global provider of market intelligence, advisory services, consulting, and events for the Packaging, Food and Beverage, Consumer Technology, Healthcare, Industrial, and Chemicals markets. With a vast team of over 400 analystsworldwide, FMI provides global, regional, and local expertise on diverse domains and industry trends across more than 110 countries. Join us as we commemorate 10 years of delivering trusted market insights. Reflecting on a decade of achievements, we continue to lead with integrity, innovation, and expertise.

The global spirometer market is set to reach a valuation of USD 616 million in 2023, with sales expected to grow at a 5.4% compound annual growth rate (CAGR), bringing the projected market size to USD 1.04 billion by the end of 2033.

Respiratory diseases rank among the top 30 causes of death globally, with chronic obstructive pulmonary disease (COPD) standing as the third leading cause. Early detection and accurate diagnosis are crucial for effective treatment, making spirometry a vital tool for assessing lung function and avoiding misdiagnosis. The growing prevalence of respiratory conditions worldwide is likely to drive demand for spirometers.

Emerging economies like India, Brazil, China, and South Africa present substantial growth opportunities for spirometer manufacturers, especially as air quality remains a major health issue. In India alone, 14 of the top 20 most polluted cities contribute to a heightened need for lung health monitoring, yet spirometer usage remains low in such regions.

Spirometry testing requires patients to blow forcefully into a mouthpiece for six seconds, with the test repeated three times to ensure accuracy. Though effective, the need for repeat tests can lengthen the procedure and may reduce patient compliance for follow-up testing.

Key Takeaways

The global spirometer market is expected to witness significant growth over the forecast period due to increasing prevalence of respiratory diseases and technological advancements.

The handheld spirometers segment is expected to dominate the market in terms of revenue share owing to their portability and ease of use.

The homecare settings segment is expected to witness significant growth due to increasing demand for convenient and cost-effective respiratory monitoring solutions.

North America is expected to hold the largest market share due to the presence of a large patient pool and advanced healthcare infrastructure.

The Asia Pacific region is expected to witness the highest growth rate due to increasing awareness regarding respiratory diseases and rising healthcare expenditure.

Key players in the market are focusing on product development and strategic partnerships to strengthen their market position.

Competitive Landscape

The competitive landscape in the spirometer market is highly fragmented, with many domestic and international players competing for market share. The market is dominated by local players, such as Jiangsu Yuyue Medical Equipment & Supply Co., Ltd., Beijing Contec Medical Systems Co., Ltd., and Wuhan HNC Technology Co., Ltd., which have a strong presence and brand recognition in the market. However, international players, such as Schiller AG, CareFusion (a subsidiary of Becton, Dickinson and Company), and Fukuda Denshi Co., Ltd., also have a significant presence in the market, and are competing for market share.

In recent years, the startup ecosystem in the market has been growing rapidly, with several new entrants entering the market with innovative and disruptive products. These startups are leveraging technologies such as artificial intelligence (AI), machine learning (ML), and cloud computing to develop new and advanced spirometry devices that offer superior accuracy, reliability, and ease of use.

Future Market Insights, Inc. (ESOMAR certified, recipient of the Stevie Award, and a member of the Greater New York Chamber of Commerce) offers profound insights into the driving factors that are boosting demand in the market. FMI stands as the leading global provider of market intelligence, advisory services, consulting, and events for the Packaging, Food and Beverage, Consumer Technology, Healthcare, Industrial, and Chemicals markets. With a vast team of over 400 analysts worldwide, FMI provides global, regional, and local expertise on diverse domains and industry trends across more than 110 countries.

The driveline additive market is expected to experience strong growth, with its value projected to reach USD 15.2 billion by 2033, expanding at a steady CAGR of 5.1% over the decade. This growth is fueled by the increasing adoption of driveline additives, which deliver enhanced performance, efficiency, and durability across a wide range of applications in both on-road and off-road vehicles. Driveline additives are gaining preference over traditional lubricant additives due to their versatile benefits, such as improved friction control, wear resistance, and optimized fuel economy, which make them essential in modern driveline systems. As the automotive industry advances with higher demands for efficiency and durability, driveline additives continue to outpace traditional additives, positioning them as crucial components in the evolving landscape of vehicle maintenance and performance enhancement.

The increasing demand for driveline additives in off-road applications in agriculture, construction, mining, and forestry heavy machinery is likely to boost the market growth. OEM requirements for extended drain, fuel efficiency, and temperature stability will create a positive market growth environment for driveline additives during the forecast period.

Engine oil additives are gaining traction in passenger cars. Motor oil additives for passenger cars can aid in reducing emissions, extending engine life, and improving performance and fuel economy, driving the market’s growth.

Environmental consciousness and regulations promoting environmentally friendly lubricants and additives can lead to developing and adopting eco-friendly driveline additives. The growth of urban populations and industrialization in emerging markets drive the demand for transportation and industrial machinery, creating opportunities for the driveline additive market.

Key Drivers of the Driveline Additive Market

Rising Consumer Focus on Fuel Efficiency: Growing awareness among consumers about fuel-saving benefits drives demand for driveline additives that enhance vehicle efficiency.

Expansion of On-Road and Off-Road Vehicle Segments: The increasing number of vehicles across both categories continues to boost sales of driveline additives to meet performance needs.

Technological Advancements in the Automotive Industry: Innovations in automotive technology emphasize the role of driveline additives in enhancing vehicle performance and longevity, fueling market growth.

Growth in Global Automotive Production: Higher production rates of vehicles globally result in greater demand for driveline lubricants and additives to ensure efficient drivetrain operations.

Expanding Global Vehicle Fleet: The rapid growth of the vehicle fleet, encompassing passenger cars, trucks, and commercial vehicles, leads to increased aftermarket and maintenance opportunities for driveline additives.

Competitive Landscape

Players have used product launches and business expansion to grow their market share, increase profitability, and stay competitive in the driveline additive market.

In recent years, prominent players have been involved in corporate tie-ups with automotive OEMs to retain their existing customers and deliver customized products. The leading players involved in the commercialization of their products to leverage immense potential in the market. Some of the recent developments in the market are discussed below.

Afton Chemical specializes in additives for fuels and lubricants, including driveline additives. They offer solutions to enhance performance, reduce friction, and improve fuel efficiency. Afton Chemical Corporation is working with OEMs to meet today’s OEM requirements for extended drain, fuel efficiency, and temperature stability.

Chevron Oronite, a subsidiary of Chevron Corporation, develops and manufactures specialty chemicals, including driveline additives, to enhance the performance and efficiency of lubricants.

Evonik is a global specialty chemical company with a focus on additives for various industries. They offer driveline additives that address friction reduction and protection of drivetrain components.

Future Market Insights offers an unbiased analysis of the global driveline additives market, providing historical data from 2018 to 2022 and forecast statistics between 2023 and 2033.

To understand opportunities in the driveline additives market, the market is segmented based on product Type (Transmission Fluid Additives, Gear Oil Additives), Application (Passenger Car, Commercial Vehicles, Off-Highway vehicles), and Region (North America, Latin America, Western Europe, Eastern Europe, South Asia and Pacific, East Asia, the Middle East, and Africa).

About Future Market Insights (FMI)

Future Market Insights, Inc. (ESOMAR certified, recipient of the Stevie Award, and a member of the Greater New York Chamber of Commerce) offers profound insights into the driving factors that are boosting demand in the market. FMI stands as the leading global provider of market intelligence, advisory services, consulting, and events for the Packaging, Food and Beverage, Consumer Technology, Healthcare, Industrial, and Chemicals markets. With a vast team of over 400 analystsworldwide, FMI provides global, regional, and local expertise on diverse domains and industry trends across more than 110 countries. Join us as we commemorate 10 years of delivering trusted market insights. Reflecting on a decade of achievements, we continue to lead with integrity, innovation, and expertise.

The global ammonium sulfate market is projected to reach an estimated value of USD 6.18 billion by 2032, growing at a robust CAGR of 7.5% from 2022 to 2032. This growth is driven by rising demand for fertilizers in the agricultural sector, where ammonium sulfate is widely used as a nitrogen and sulfur source to improve crop yields. The market expansion is also influenced by increasing industrial applications in food processing, water treatment, and pharmaceuticals. Furthermore, the demand for ammonium sulfate is expected to benefit from sustainable farming practices and the increasing global emphasis on food security, supporting its upward trajectory over the forecast period.

The demand for ammonium sulphate in Europe is witnessing a significant uptick, driven primarily by its applications in wood preservation and water treatment. As the need for wood products continues to rise, particularly in construction and woodworking, the demand for effective wood preservatives is growing correspondingly. Ammonium sulphate is recognized for its hygroscopic properties, which make it an essential ingredient in many wood preservation formulations. Furthermore, its role as a fire retardant—elevating combustion temperatures and enhancing residue formation—further fuels market interest. As safety regulations tighten and the demand for durable wood products increases, the ammonium sulphate market is poised for substantial growth.

In addition to wood preservation, the escalating scarcity of clean water resources is driving the adoption of effective water treatment solutions. When combined with chlorine, ammonium sulphate acts as a potent disinfectant, making it valuable in municipal water treatment facilities. The rising demand for improved water quality and sanitation practices across Europe will significantly contribute to the growth of the ammonium sulphate market. Additionally, the Fertility Application Ordinance Act in Germany, which promotes sustainable agricultural practices, aims to boost crop yields and enhance soil quality through targeted fertilization strategies. This regulatory framework will create a favorable environment for the increased utilization of ammonium sulphate, further reinforcing its demand in the European market over the coming decade.

Key Drivers Fueling the Ammonium Sulphate Market:

Rising Agricultural Demand for Fertilizers: Ammonium sulphate is widely used as a nitrogenous fertilizer to enhance crop yield and soil quality. With the global population increasing and the demand for food security rising, farmers are increasingly adopting ammonium sulphate to boost agricultural productivity.

Expanding Industrial Applications: Beyond agriculture, ammonium sulphate finds applications in industrial processes such as water treatment, textiles, and pharmaceuticals. Its use as a food additive and in flame retardants further broadens its market scope, contributing to steady demand.

Growing Preference for Sulphur-Containing Fertilizers: As sulphur deficiencies in soil become more common due to the widespread adoption of sulphur-free fertilizers, ammonium sulphate is being preferred for its dual role in supplying both nitrogen and sulphur. This trend is particularly strong in regions with intensive agricultural practices, such as North America and Europe.

Stringent Environmental Regulations: Environmental regulations promoting the use of eco-friendly fertilizers are pushing the adoption of ammonium sulphate. The compound’s lower environmental impact compared to other nitrogen fertilizers makes it a preferred choice in regions with strict environmental policies.

Supportive Government Initiatives: Governments in various countries are providing subsidies and support for sustainable farming practices. This includes the adoption of ammonium sulphate fertilizers to improve soil health and crop yield, which is encouraging market growth.

Challenges Constraining the Ammonium Sulphate Market:

Price Fluctuations of Raw Materials: The cost of raw materials required to produce ammonium sulphate, such as sulphur and ammonia, can be volatile. Fluctuating raw material prices directly affect production costs, thereby impacting the overall profitability of ammonium sulphate manufacturers.

Competition from Other Nitrogenous Fertilizers: Despite its benefits, ammonium sulphate faces stiff competition from other nitrogen-based fertilizers like urea and ammonium nitrate. These alternatives often have higher nitrogen content and are available at a lower cost, making them a preferred choice for many farmers.

Environmental Concerns over Excessive Nitrogen Use: While ammonium sulphate is beneficial for crop yield, excessive use can lead to environmental issues like soil acidification and water pollution. Regulatory bodies are imposing restrictions on nitrogen fertilizer usage, which may hamper market growth.

Supply Chain Disruptions: The production and distribution of ammonium sulphate are susceptible to supply chain disruptions, especially in regions dependent on imports for raw materials. Geopolitical tensions and trade restrictions can further exacerbate these supply challenges.

Technological Advancements in Fertilizer Alternatives: Continuous innovation in fertilizer technology is leading to the development of new products that offer better efficiency and environmental benefits. The advent of slow-release fertilizers and bio-based products is putting additional pressure on the ammonium sulphate market.

Market Competition

Key players in the ammonium sulphate market are Koninklijke DSM N.V. (Fibrant), JSC KuibyshevAzot, UBE Industries Ltd, Toray Industries Inc., China Petrochemical Development Corporation, China Petroleum & Chemical Corporation (Sinopec Corp.), JSC “Grodno Azot”, Grupa Azoty, Domo Chemicals, Gujarat State Fertilizers & Chemicals Ltd, Sumitomo Chemical, Evonik Industries AG

In August 2022, JSC “Grodno Azot” announced that it will be partially limiting the production of nitrogen fertilizer due to the increase in prices of natural gas.

DOMO Chemicals, a key player in the ammonium sulphate market is focusing on producing the same sustainable and reducing their overall carbon footprint.

Leading Players in the Market

Koninklijke DSM N.V. (Fibrant)

JSC KuibyshevAzot

UBE Industries, Ltd

Toray Industries Inc

China Petrochemical Development Corporation

China Petroleum & Chemical Corporation (Sinopec Corp.)

JSC “Grodno Azot”

Grupa Azoty

Domo Chemicals

Gujarat State Fertilizers & Chemicals Ltd.

Sumitomo Chemical

Evonik Industries AG

About Future Market Insights (FMI)

Future Market Insights, Inc. (ESOMAR certified, recipient of the Stevie Award, and a member of the Greater New York Chamber of Commerce) offers profound insights into the driving factors that are boosting demand in the market. FMI stands as the leading global provider of market intelligence, advisory services, consulting, and events for the Packaging, Food and Beverage, Consumer Technology, Healthcare, Industrial, and Chemicals markets. With a vast team of over 400 analystsworldwide, FMI provides global, regional, and local expertise on diverse domains and industry trends across more than 110 countries. Join us as we commemorate 10 years of delivering trusted market insights. Reflecting on a decade of achievements, we continue to lead with integrity, innovation, and expertise.